Today, SpaceX agreed to buy Anysphere — the maker of AI coding tool Cursor — for $60 billion. Not a typo. Sixty billion dollars for a startup that helps developers write code faster.

Bloomberg, CNBC, The Verge, WSJ, and CNA all confirmed the deal on June 16, 2026. SpaceX filed with the SEC. Cursor investors get SpaceX stock based on the $60 billion price. This is not a cash deal. And that distinction changes everything.

Sponsor

Have you tried Elon Musk’s new AI agent?

It’s the most powerful AI ever created.

Musk himself thinks it could make investors 70 times their money.

In a few short years…

I expect an announcement from Musk by the end of this month… (S'ouvre dans une nouvelle fenêtre)

That will make this AI agent available to every American.

And I’ll show you how to get in right away, on the ground floor.

Click here to watch the live demo. (S'ouvre dans une nouvelle fenêtre)

The Anatomy of a $60 Billion Stock Swap

SpaceX just went public in a historic Nasdaq debut, with its valuation topping $2 trillion. When you pay $60 billion using newly printed public stock, the real cost depends entirely on where that stock trades later. If SpaceX stock rises 20% by close, the dilution is relatively cheap. If it drops 20%, Musk overpaid by $12 billion in real terms. The deal’s currency is shaky by nature.

This transaction did not pop up overnight. In April, SpaceX locked in an option: buy Cursor for $60 billion, or pay a massive $10 billion breakup fee. A $10 billion walk-away cost is unprecedented in tech history. It proves SpaceX was desperately driven, and Cursor held immense leverage during negotiations.

SpaceX deliberately waited until after its Nasdaq IPO to execute. The playbook is classic: go public first, establish your stock as a highly valued currency, and then use it to fund aggressive acquisitions. The tactic is old. The scale, however, is not.

Per CNBC, SpaceX claims the deal aims to “bolster its presence in the enterprise AI sector.” Notably, Musk openly voiced dissatisfaction with the coding solutions offered by xAI, admitting they do not measure up to popular alternatives like Claude Code and Codex. He merged xAI into SpaceX in February 2026, and is now spending $60 billion to fix his own AI team’s shortcomings.

The Ledger Brief

SpaceX locks in $60 billion Cursor deal to power AI coding push (S'ouvre dans une nouvelle fenêtre) (Yahoo Finance)

Struggling Pizza Hut restaurant chain will be sold for $2.7 billion (S'ouvre dans une nouvelle fenêtre) (Yahoo Finance)

The ‘Magnificent 7’ is so last year. SpaceX, OpenAI, and Anthropic are ushering in the FAB 10. (S'ouvre dans une nouvelle fenêtre) (Yahoo Finance)

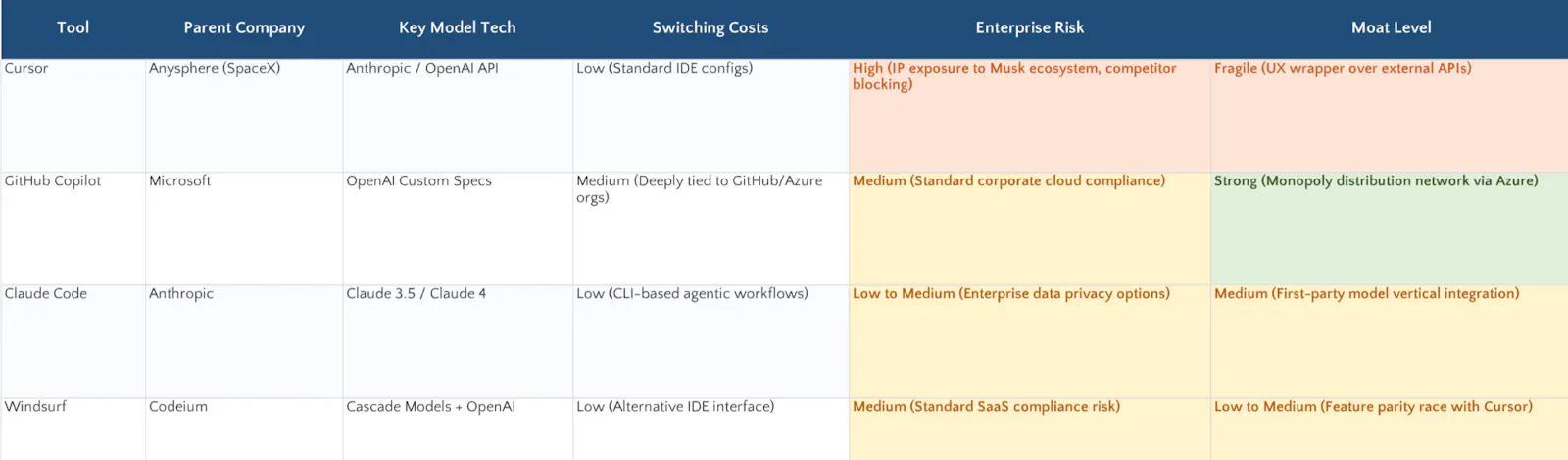

The Rivals and the “Vibe Coding” Illusion

The market for AI coding tools is highly congested. Cursor is fighting head-to-head with heavily backed giants.

Cursor’s rapid rise was fueled by the “vibe coding” trend, where developers build software using plain-language prompts. While the shift is real and saves hours on boilerplate, the tailwind lifts all boats. A rising industry tide is not a unique competitive moat.

The core vulnerability here is switching costs. They are incredibly low. A development team can easily swap from Cursor to Claude Code or Copilot in a single afternoon. A $60 billion valuation requires ironclad user retention, which is exceptionally difficult to maintain in a browser-and-editor market.

Without Anysphere’s audited books, we must run the math on estimated seats. Cursor charges roughly $20/month per user. If they somehow captured 5 million paying developers—a massive chunk of the global dev base—yearly revenue would sit around $1.2 billion.

At a $60 billion acquisition price, SpaceX is paying a staggering 50x revenue multiple. For context, Salesforce trades around 8x revenue, and Snowflake trades at 15–20x. A 50x multiple requires hypergrowth with permanent moats, which Cursor simply has not proven yet.

The xAI Sprawl and the Bull Case

The deal could give xAI a stronger foothold in the coding market while providing Cursor with massive compute clusters. The combined Musk group now spans rockets, social media, LLMs, and developer tools. Historically, public markets punish such corporate sprawl with a conglomerate discount.

To justify this price tag, the bullish case relies on three strict pillars:

Enterprise Lock-in: Cursor must secure multi-year, site-wide developer contracts with Fortune 500 firms.

Custom Models: Their fine-tuned models must maintain a clear, measurable quality edge over vanilla APIs.

Workflow Stickiness: The IDE environment must become deeply woven into enterprise deployment pipelines.

If these pillars fail, SpaceX is essentially buying a wrapper with high churn risks. The connection with xAI’s computing power is a double-edged sword.

[ xAI Compute Surplus ] ──► Forced Switch to Grok ──► Quality Drops ──► Dev ChurnIf SpaceX forces Cursor to abandon Anthropic and OpenAI models in favor of Grok, the developer experience could degrade rapidly. Users will not hesitate to migrate to rival platforms.

Portfolio Risk and the 90-Day Playbook

For SpaceX shareholders, the dilution math is straightforward. A $60 billion purchase against a $2 trillion valuation represents roughly 3% dilution. If the stock dips post-IPO, the real cost of the acquisition escalates. I do not hold SpaceX stock, and I am watching this unfold with zero rush. Patience is free; FOMO is expensive.

If your engineering team currently uses Cursor, this acquisition introduces immediate platform risks. You must audit three key areas before the Q3 2026 close:

Data Privacy: Cursor reads your proprietary codebase to generate suggestions. Under SpaceX and xAI ownership, you must verify who retains access to this data.

Model Quality: Track whether the tool remains model-agnostic or is forced into the xAI ecosystem.

Contract Locks: Prepare for potential price hikes by locking in enterprise rates under your current terms.

The 90-Day Checklist

[ ] Monitor SpaceX’s first 10-Q filing for hidden Cursor segment revenue data.

[ ] Audit changes to Cursor’s Terms of Service regarding data training.

[ ] Watch rival feature launches from GitHub Copilot and Anthropic’s Claude Code.

[ ] Track talent retention at Anysphere; key engineers often exit after mega-mergers.

Sixty billion dollars is a wild price for an editor. It might be a stroke of genius, or it might be AOL-Time Warner in a hoodie. We lack the private books to know for sure. But we now have the exact framework to judge it as the data leaks out.

Watch the filings. Skip the hype.

Feedback Loop: Rate Today’s Ledger

We strip away the hype to focus purely on market plumbing and capital flows, but we want to ensure our analytical depth matches your portfolio needs.

Hit reply to this email right now and type a single number (1, 2, 3, or 4) to share your rating:

1 — Highly valuable: This level of structural macro analysis is exactly why I subscribe.

2 — Informative, but needs more execution: Strong perspective, but I want to see specific tickers or tactical setups included next time.

3 — Disagree with the premise: The breakdown feels overly pessimistic and underestimates the long-term strategic monopoly of the asset.

4 — Solid read: A well-balanced perspective to chew on. Keeping a cool head and waiting for the next drop.

Want to expand on your vote?

Don't stop at just a number. If you have a counter-thesis, a specific question, or want to challenge our logic, type it directly into your reply. We read every single response, and the sharpest macro insights from our community will be featured and deconstructed in our next brief.

Date

16/06/2026