Small floats, index-buying spirals, and retirement nest eggs — read this briefing before day one.

Real market analysis starts exactly where the public relations narratives break down. Corporate treasuries and underwriting syndicates routinely hide structural vulnerabilities under the guise of “strategic growth optimization,” using media hype to mask raw capital strain. When Elon Musk’s SpaceX prepares a public debut targeting a valuation of at least $1.8 trillion, market sentiment becomes completely irrelevant. We ignore the cheerleading commentary and audit the cold, immutable data inside the underwriting mechanics.

This isn’t a speculative prediction on the future of space exploration. It is a cold look at verified financial data points. The numbers reveal a structural divergence between manufactured retail demand and institutional exit strategies. If your retirement income depends on unencumbered capital, this is the exact type of macro-event you must dissect before it costs you capital. The numbers are too large to dismiss, and the pattern is too clear to ignore.

1. The Numbers Behind the Hype: Valuation Built on Ambition

Let let be entirely direct: SpaceX’s target of $1.8 trillion is staggering, especially when you calculate how much of this capital structure rests on forward-looking “rocket ambitions” rather than present free cash flow. This valuation model reflects aggressive expectations about multi-decade revenue trajectories rather than current fundamental balance sheet health, highlighting a massive delta between headline narrative and underlying financial reality.

The underwriting syndicate has already deployed its institutional marketing machinery. Jamie Dimon recently hosted a closed-door investor symposium at JPMorgan Chase’s global headquarters specifically to structure the institutional books for this deal. However, in my years analyzing corporate balance sheets, I’ve noted one absolute rule: the presence of tier-one institutional gatekeepers does not guarantee a bargain for retail participants.

The underlying structure of this multi-billion-dollar offering suggests that early demand is being systematically manufactured rather than organically driven. For any Individual Sovereign running a lean portfolio, recognizing how this demand is engineered is crucial for isolating the real balance sheet risks before day one.

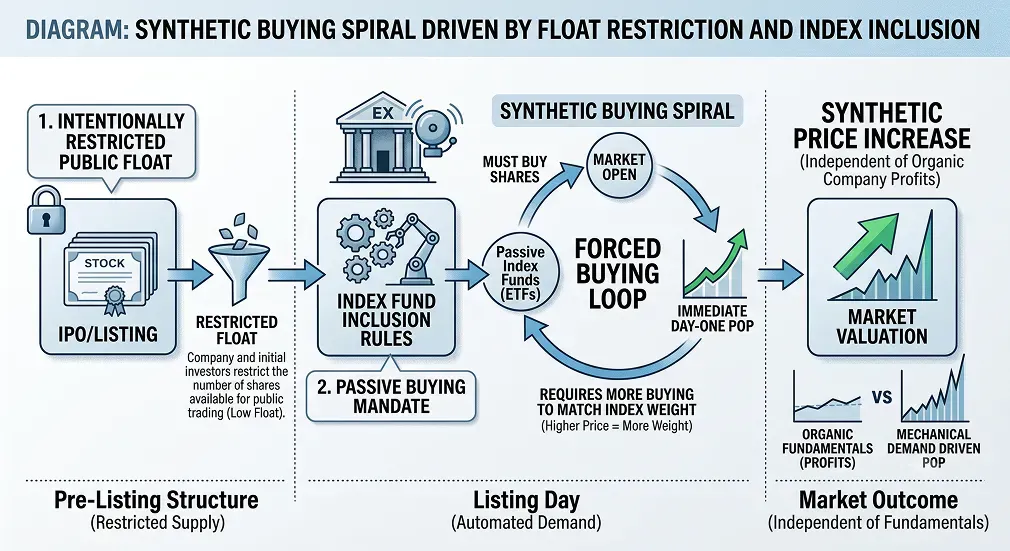

2. The Mechanics That Manufacture a Pop: Scarcity and Index Manipulation

The mechanics of a mega-cap IPO can significantly distort initial market performance, completely decoupling a stock’s price from its organic business operations.

Underwriters frequently deploy specific operational levers to manipulate early price action:

The Restricted Public Float: By releasing only a microscopic percentage of total equity to the public on day one, underwriters create intense artificial scarcity. This thin order book means even moderate buying volume can trigger a massive upward price spike.

Forced Index Rebalancing: Under typical listing modernizations, index providers can shorten waiting periods for massive listings. This forces passive index funds and ETFs to automatically acquire millions of shares to match index weights, completely irrespective of the underlying company’s actual P/E ratio or cash-flow generation.

Aggressive Acceleration of Lockup Expirations: While insiders are typically restricted from liquidating their equity immediately, modern underwriting structures frequently include staggered or performance-accelerated lockup releases. If the stock trades above a specific target for a mere 15 business days, the insider exit door opens early.

As a result of this design, initial public demand is heavily subsidized by retail market participants and passive index trackers who lack the informational advantages of early-stage venture syndicates. Retail capital risks stepping directly into a liquidity trap, buying equity at an artificial premium while insiders quietly position for an exit.

3. The Contrarian Read: When Hype Masks Exit Liquidity

The multi-trillion-dollar headlines intentionally bury the structural purpose of this offering: this deal is not engineered to maximize returns for the retail participant buying the opening bell. It is designed to provide massive, unencumbered liquidity to early-stage insiders, private equity funds, and venture backers who have had their capital locked up for years.

To understand how this capital migration unfolds across the go-live week, we must map out the exact structural scenarios supported by institutional data.

4. Three Scenarios for the Week Ahead: Modeling the Settlement Path

To insulate your capital from emotional decision-making, we model the post-listing path across three distinct operational templates:

The Synthetic Bull Case

Strong retail momentum and mandatory institutional index-tracking purchases easily overwhelm the small public float. The stock pops aggressively on day one. While this scenario satisfies television commentators, it represents the highest risk profile for a self-directed nest egg. Buying into this artificial momentum means acquiring equity at the absolute apex of manufactured scarcity.

The Base Case Drift

The stock holds an elevated range short-term due to the initial index-buying mandate. However, as the initial excitement stabilizes, the reality of forward-looking cash flow catches up with the multiple. As accelerated lockups cross their performance thresholds, early insiders execute their liquidation strategies, creating an unyielding supply overhang that retail capital is forced to absorb.

The Structural Bear Case

The initial marketing narrative cools, and the market forces a brutal re-rating toward present fundamental metrics. If insiders liquidate their positions rapidly to lock in gains, the initial pop completely reverses, leaving late-stage buyers holding a highly volatile asset whose capital structure is heavily exposed to execution risks.

5. Why a Day-One Pop Could Cost Your Nest Egg: The Sovereign Directive

Own a piece of a world-changing technology company is a legitimate long-term aspiration, but owning it at any price is an operational failure. For self-directed investors focused on building an independent cash-flow stream, capital preservation is the absolute mandate.

If you are evaluating exposure to this listing, apply these ironclad risk parameters:

Enforce Strict Position Sizing: Never allocate more capital than you can afford to see impaired during a structural re-rating. Treat any initial allocation as speculative venture capital.

Audit Your Broker’s Flipping Restrictions: Before submitting an Indication of Interest (IOI), verify the exact penalty parameters. Many retail platforms block participants from future offerings if shares are sold within 30 days of the debut.

Embrace the “Wait-and-See” Framework: Waiting for the 90-day post-IPO stabilization period to clear is a highly sophisticated institutional strategy. It allows the artificial float scarcity to normalize and reveals the stock’s true fundamental floor.

The financial system was engineered to use retail capital as exit liquidity for late-stage private equity. When boardroom underwriters deploy structural scarcity to mask extreme forward valuations, your only real defense is mathematical discipline. If you know a peer currently considering allocating a portion of their hard-earned nest egg into this debut, deliver this data to them before the opening bell. The structure is the real story—and it’s the exact part the hype leaves out.

Datum

09.06.2026