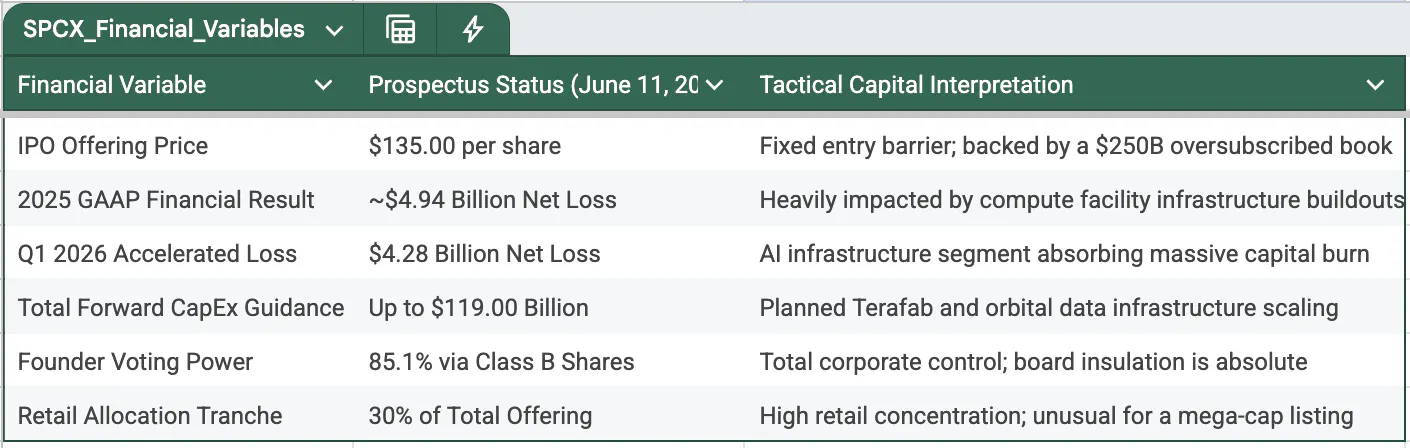

Tomorrow, June 12, 2026, SpaceX officially opens public trading on the Nasdaq under the ticker SPCX. The transaction parameters are locked at a fixed price of $135 per share, targeting a historic gross primary raise of $75 billion across 555.6 million Class A shares. This establishes an implied market capitalization between $1.75 trillion and $1.77 trillion at the opening bell.

If the deal clears at this level, Elon Musk's personal net worth mathematically crosses $1 trillion, cementing his status as the first official trillionaire in recorded history. The media is running its standard playbook: breathless commentary on visionary multi-planetary expansion and retail buyer lines stretching across brokerage apps from Sydney to New York.

Let me speak with absolute corporate candor. Elon Musk as a governance counterparty is highly erratic, hyper-politicized, and fundamentally hostile to minority shareholder input. But as a self-directed sovereign investor, your capital does not run on personal liking or corporate morality. It runs on structural positioning. The establishment wants you to buy into the mythology; your actual objective is to figure out if you can safely extract a slice of this massive, government-backed infrastructure pie.

Sponsor

Breaking news,

Apple just secretly added Starlink satellite support to iPhones through iOS 27.

One of the biggest potential winners?

Mode Mobile. (Abre numa nova janela)

(Abre numa nova janela)

(Abre numa nova janela)Just about everything Elon touches turns to gold:

SpaceX projected IPO at $1.75T

Tesla up 30,000% since IPO

And now - every iPhone gets satellite access

But while Wall Street focuses on Apple, Mode Mobile is quietly positioned to capitalize on this global satellite revolution.

Their EarnPhone technology already:

Reaches 490M+ users worldwide

Helped those users save and earn $1B+ million

Grew revenue 32,481%

And that was before global satellite coverage.

With Apple-SpaceX eliminating "dead zones" worldwide, Mode's earning technology can reach 3B+ unbanked people globally in rural populations worldwide.

We’re talking about emerging markets with no infrastructure.

And right now, you can still invest at $0.52/share before their potential IPO (Abre numa nova janela)

Over 59,000+ shareholders have already claimed their shares and they’ve just secured the $MODE ticker from Nasdaq. The time to invest is now, before any potential IPO.

Invest in Mode Mobile and earn your stake in this $1 trillion industry. (Abre numa nova janela)

(*ad)

1. The Political Infrastructure Behind the Valuation

To evaluate this $1.77 trillion asset accurately, an Individual Sovereign must look past the consumer branding and identify the underlying cash-flow driver: SpaceX operates essentially as an unassailable federal procurement contractor. The entity pulls in roughly $3 billion per year from NASA, the Department of Defense, and the Space Force, locking down a functional monopoly on domestic heavy-payload launch capabilities.

The amended S-1 registration statement reveals a highly complex capital architecture, heavily transformed by the February 2026 vertical merger with xAI:

The core data confirms that this entity is structurally pre-profit on a GAAP basis and faces staggering capital deployment demands. Yet, the revenue lines are insulated by deep political ties. Bloomberg tracking data indicates that at least ten administration officials retain personal stakes in SpaceX and xAI worth up to $44 million combined, insulated via ethics waivers. The state is not merely regulating this enterprise; it is actively anchored on its cap table.

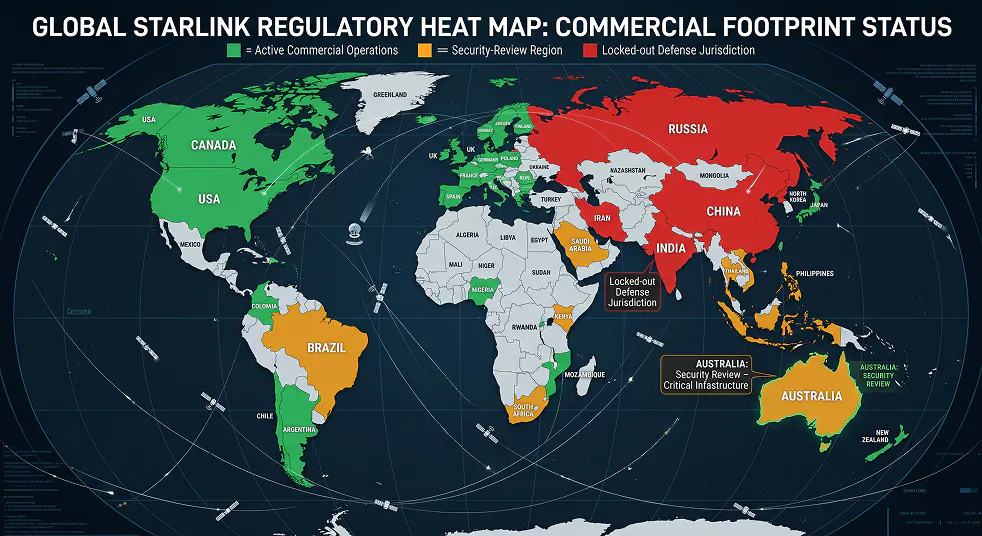

2. The Starlink Sovereignty Conflict

The second critical risk layer involves international regulatory pushback against Starlink’s global footprint. Mainstream retail analysis completely ignores the national security friction surfacing across foreign defense complexes.

On June 10, declassified Australian Department of Home Affairs documents confirmed that defense officials are flagging severe infrastructure availability risks due to Starlink's offshore custody. Concurrently, India’s Ministry of Home Affairs has frozen final Starlink operating licenses, withholding clearances until the network guarantees complete adherence to localized data interception and local security rules during regional crises.

While these regulatory blockades temporarily restrict access to major consumer internet markets, SpaceX has successfully offset international friction by securing deep enterprise infrastructure moats. The June 3 S-1 amendment disclosed a staggering Cloud Service Agreement with Alphabet, where Google has legally contracted to pay SpaceX $920 million per month through June 2029 to lease custom GPU clusters. Combined with Anthropic’s $1.25 billion monthly commitment at the Colossus 1 facility, SpaceX has secured an annualized, recurring commercial pipeline of over $26 billion that remains entirely independent of standard consumer retail metrics.

3. The 13-Word Dilution Trigger: Managing Governance Risk

The ultimate structural risk buried inside page 51 of the June 3 amendment is an explicit, revised disclosure warning: "We may issue a significant amount of equity in connection with future transactions." This is not boilerplate language. Institutional desks are actively pricing this as a clear signal that Musk intends to use the hyper-inflated, post-IPO equity of SpaceX as a highly liquid acquisition currency.

With Musk commanding 85.1% voting control through Class B shares, public stockholders have zero corporate governance mechanisms to block dilutive maneuvers. If the board decides to execute a massive, share-dilutive merger to absorb other distressed elements of Musk's corporate ecosystem—such as a structural consolidation with Tesla—minority equity holders will absorb the immediate supply shock with no legal recourse. The corporate structure is engineered to extract public market liquidity while denying public market control.

4. The Sovereign Directive

For Individual Sovereigns focused on long-term capital preservation, this historic listing demands absolute tactical precision over emotional bias.

First, I am not chasing the open-market listing at $135 tomorrow morning. The underwriting syndicate has engineered a highly insulated trading environment. By releasing a minute 4% public float and utilizing Nasdaq's updated 15-day fast-track indexing rules, the banks will force massive passive index funds (like the QQQ) to mechanically purchase up to 30% of the available shares by late June. This creates an artificial, institutional buying floor that protects the $135 level, but it means you are buying a tightly managed supply loop rather than an organic free market.

Second, understand the passive capture architecture. If you hold a standard Nasdaq-100 index vehicle or retirement growth fund, your ledger is already automatically buying SpaceX today. The passive indexing parameters ensure your capital is taking its slice of the pie at the $135 strike whether you place an active order or not. There is no strategic reason to duplicate that identical exposure in your active brokerage account.

Third, wait for the artificial floor to clear before deploying unhedged capital. Independent valuation models from desks like Morningstar calculate the core fundamental value of the standalone aerospace and connectivity assets closer to $780 billion, or roughly $60 per share.

Let the forced index fund buying run its course over the next 15 sessions. Let the insiders execute their initial liquidity events, and let the market begin pricing the dilutive acquisition risks. Our tactical window opens only when the initial roadshow euphoria fades, the political backstops are thoroughly stress-tested, and the math offers an organic entry point that allows us to safely harvest our piece of the infrastructure cash flow on our own terms.

Please read the offering circular (Abre numa nova janela) and related risks at invest.modemobile.com (Abre numa nova janela) . This is a paid advertisement for Mode Mobile’s Regulation A+ Offering.

Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur.

The Deloitte rankings are based on submitted applications and public company database research, with winners selected based on their fiscal-year revenue growth percentage over a three-year period.

Pro forma revenue and EBITDA, includes full year numbers of the businesses acquired throughout 2025.

Disclaimer: This analysis is for educational purposes only and should not be considered investment advice. Always do your own research before making investment decisions.

Items marked with an asterisk (*) are promotional and help support this newsletter at no cost to readers.

Data

11/06/2026