Hunting plc – listed on the London Stock Exchange under the ticker symbol HTG.L – is not a name that comes up in everyday conversation. Yet this British company operates in a niche that is indispensable for global energy supply: the manufacture and distribution of highly specialized components for the oil and gas industry, and increasingly for the defense sector. Pipes, fittings, drilling tools – products without which no well can function and no offshore platform can operate safely.

The company: A silent enabler of the energy industry

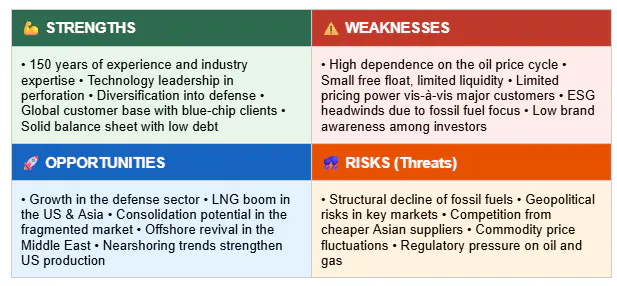

Founded in 1874, Hunting has reinvented itself time and again over the past 150 years. Today, the company is divided into three main segments: Hunting Titan (perforation technologies), Advanced Manufacturing (precision components), and its traditional oilfield services business. Of particular interest is its strategic diversification into the defense sector: In a world where NATO countries are significantly increasing their military spending, Hunting is positioning itself as a supplier of precision-manufactured components – a lever that has received little attention from analysts to date.

The company has a global presence with locations in the USA, the Middle East, Asia, and Europe. Its customer base includes almost all major energy companies: ExxonMobil, Shell, BP, and Saudi Aramco. This creates a degree of predictability, but also a structural dependence on a sector that is currently undergoing enormous pressure to transform.

Recent developments: Between cycle and structural change

Fiscal year 2025 went better than many had expected for Hunting. Demand for oil and gas equipment remained robust, driven by persistently high energy prices and the realization that the energy transition is taking longer than politically desired. Hunting was able to stabilize its revenue and improve margins – a sign that the cost-cutting programs of previous years are bearing fruit.

Of particular note is the expansion of the TITAN segment. Its perforation products are considered technologically advanced and are in high demand in North America, the world's largest market for shale oil drilling. The boom in LNG exports from the US is generating additional order volumes. At the same time, Hunting has begun expanding its manufacturing capacity for defense applications – a move that could reduce cycle dependency in the medium term.

The repurchase of $40 million of its own shares signals that management considers the current valuation attractive. With the share price significantly below its historical high, the company apparently sees more value in itself than in alternative investment opportunities.

SWOT analysis: Strengths, weaknesses, opportunities, threats

The moat: What separates Hunting from the competition

Hunting's competitive advantage lies in a combination of technological expertise, certifications, and established customer relationships. Those who have equipped their wells with Hunting titanium perforation charges don't switch suppliers lightly. The quality requirements in oil and gas production are simply too high – a component failure can cause billions in losses. Furthermore, years of API certifications and specific qualifications for high-pressure/high-temperature applications make it difficult for newcomers to enter the market.

The defense industry is building a second competitive moat: arms contracts typically run for many years, require intensive qualification processes, and are state-controlled. Once someone is in the system, they often stay there for a long time.

Critical conclusion: Substance, but not a sure thing.

Hunting plc is a well-managed niche company with a real competitive advantage and a sound strategy. The share buyback is a positive signal – but not a guarantee of success. The structural risks in the oil and gas industry are real. Those who believe the energy transition will proceed more slowly than expected and that the oilfield services market will continue to grow will find Hunting an attractive entry point. Those who anticipate accelerated structural change should remain skeptical. The diversification towards defense is promising, but still too small to significantly alter the overall picture. Hunting is a stock for patient investors – and for those willing to ride out market cycles.

Datum

06.03.2026

0 Kommentare

Möchtest du den ersten Kommentar schreiben?

Werde Mitglied von Dividend Growth Stocks🚀 und starte die Unterhaltung.