November 2022

With the Russian invasion of Ukraine and the following full scale military conflict, the context of Europe´s energy policy changed significantly. The war illustrates Europe’s dependency on energy imports, not at least gas, and how vulnerable regional economies are to shocks in commodity markets.

Firms depending on gas or high energy inputs for their production are particularly challenged by increasing energy prices and the expected energy crisis. The impacts are also clearly felt by citizens, not at least due to inflation which in particular hits households with lower incomes and those already at risk of poverty.

Most of the European analysis of impacts of the war are at macroeconomic or national level. Among others, a first assessment of the national vulnerabilities to impacts of the war in the European economic forecast (summer 2022) (S'ouvre dans une nouvelle fenêtre), focuses on energy, trade & value chains and assets at national level. Latvia, Estonia, Bulgaria, Lithuania, Czechia, Slovakia, Hungary, Poland, Slovenia, Cyprus, Croatia and Greece are the most affected countries. Focusing on the vulnerability of firms, the EIB (S'ouvre dans une nouvelle fenêtre) estimates particularly high stress levels for Lithuania, Greece, Latvia, Poland, Hungary, Croatia and Spain.

Regional energy dependencies

Further developing this to address regional rather than national vulnerabilities requires a broader understanding of sensitivities to the effects of the war. Earlier this summer we made a first attempt to assess regions’ sensitivities to the impacts of the war, taking into account their socio-economic profile and energy dependencies. For more details see our studies for the European Committee of the Regions (S'ouvre dans une nouvelle fenêtre) and the European Parliament (S'ouvre dans une nouvelle fenêtre).

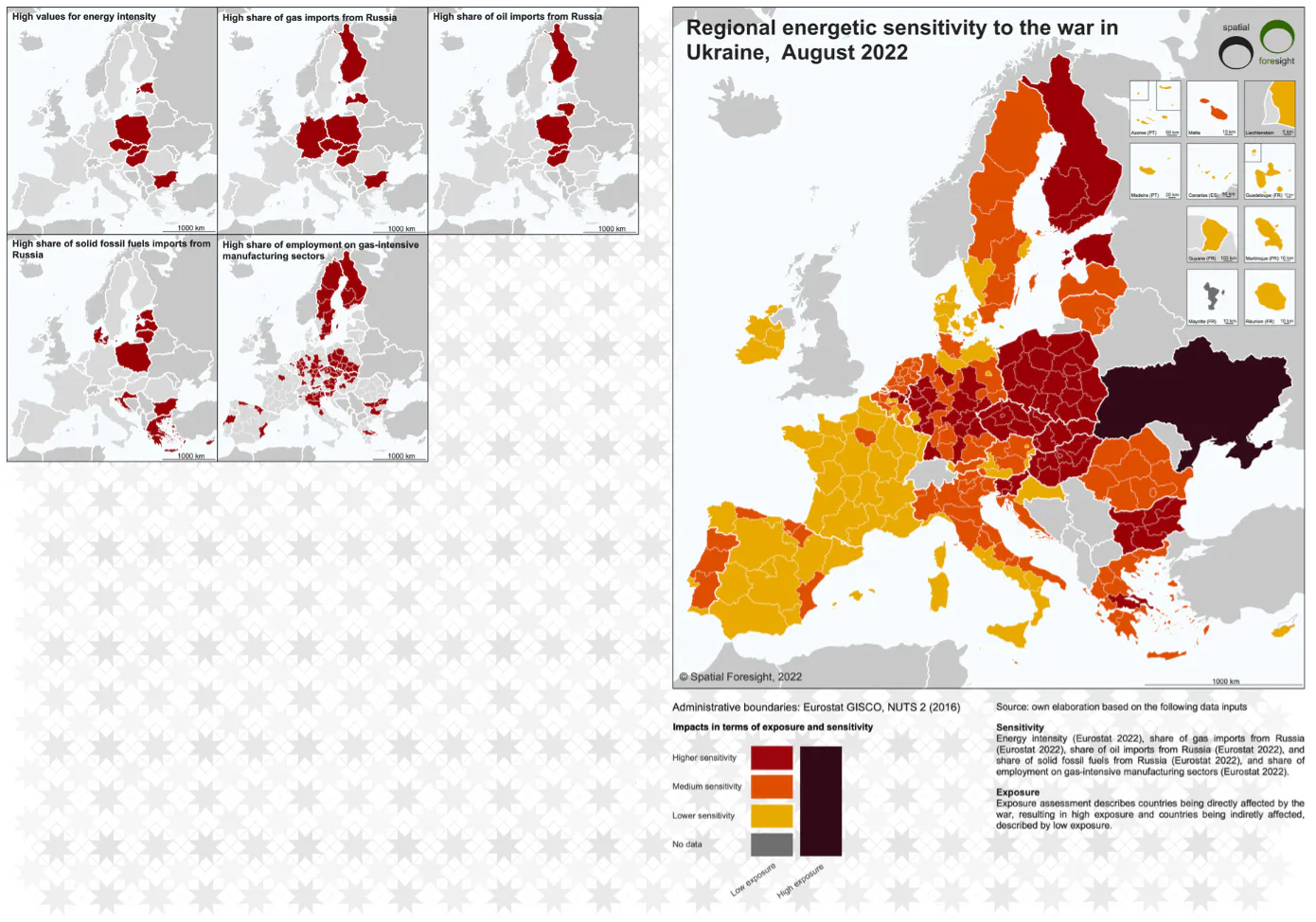

To better understand which regions in Europe are particularly affected by this, we looked into five sensitivity indicators, unfortunately not all of them allowed for analysing regional data:

Employment in energy-intensive manufacturing sectors, i.e. the share of people working in fields of coke and refined petroleum products, chemicals and chemical products, basic metals, paper and paper products, and non-metallic minerals. These are the five most energy-intensive manufacturing industries according to a recent OECD study (S'ouvre dans une nouvelle fenêtre). The most sensitive regions are to be found in Finland, Sweden, Poland, Czechia, Slovakia, Austria, Hungary, Bulgaria, Italy, Slovenia, Germany, as well as some regions in Greece, Spain, Portugal, Belgium and France.

Energy intensity, i.e. the amount of energy required to produce 1 EUR in added value varies across industries. Increasing energy prices and risks of energy shortage affect highly energy intensive industries, e.g. heavy industries. Estonia, Poland, Czechia, Hungary, Slovakia, Bulgaria and also in Malta have the highest energy intensity for industry.

Share of gas imports from Russia, i.e Europe’s dependency on imports of Russian gas prior to Russia´s war on Ukraine. Two fifths of the gas that Europeans burned in 2021 came from Russia. Germany, Poland, Slovakia, Czechia, Latvia, Hungary, Bulgaria and Finland had the highest shares of Russian gas.

Share of oil imports from Russia. Prior to the war, Russia was the largest global oil exporter, and the EU was the largest buyer of Russian oil. This brought additional pressure to diversify, an urgency to find replacements. The most affected countries are Finland, Hungary, Lithuania, Poland and Slovakia.

Share of solid fossil fuel imports from Russia. Russia is also an exporter of coal and fossil fuels. Although the EU has taken steps towards phasing out solid fossil fuels as part of its green transition, the war brought additional pressure to replace Russian imports. This mainly affected countries with higher shares of coal imports coming from Russia, such as Bulgaria, Cyprus, Denmark, Estonia, Greece, Croatia, Lithuania, Latvia and Poland.

Bringing together these sensitivities, the map shows a combined energy-related negative sensitivity index. In this combined index, Poland is most sensitive to the energy crises. This is followed by Bulgaria, especially due to high energy intensity and a high share of gas and solid fossil fuels imports from Russia. Finland has a high share of gas and oil imports from Russia, and a high share of employment in energy-intensive manufacturing sectors. Other highly sensitive places are in Greece, Slovenia, Hungary, Slovakia, Czechia, Germany and Estonia.

The least sensitive regions are in Ireland, Spain, France, the region around the Tyrrhenian Sea in Italy, Cyprus, Zagreb region in Croatia, parts of Austria, the north of Germany, all of Denmark, and regions around Stockholm and Gothenburg in Sweden.

The results can also be read in terms of different types of regions. In rough terms, outermost regions are the least sensitive to energy supply changes, followed by island regions, with median values far below the EU average. Border regions, on the other hand, are the most sensitive type of regions.

With regards to the regional types underpinning EU cohesion policy, less developed regions are the most sensitive to energy supply changes. Transition regions, on the other hand, are the least negatively sensitive.

Further details of this discission, also addressing other sensitivities to the war in Ukraine, can be found in studies to the European Parliament (S'ouvre dans une nouvelle fenêtre) and the European Committee of the Regions (S'ouvre dans une nouvelle fenêtre).

by Kai Böhme

https://steadyhq.com/en/spatialforesight/posts/499e2eee-886e-4ebe-9a41-ff752327ea1f (S'ouvre dans une nouvelle fenêtre)

Date

04/11/2022

Sujet

Resilience & transition

0 commentaire

Vous voulez être le·la premier·ère à écrire un commentaire ?

Devenez membre de spatialforesight et lancez la conversation.