Monday’s opening bell delivered a brutal reality check to global investment strategies. Following a sharp weekend escalation in the Middle East, WTI crude surged past $94 a barrel, while the global benchmark Brent rapidly approached $98.

This is not a typical cyclical demand rally signaling healthy economic expansion; we are witnessing a classic, aggressive supply-side shock hitting the planet’s primary logistical choke point—the Strait of Hormuz. Because Western commercial stockpiles and the Strategic Petroleum Reserve (SPR) have been thoroughly depleted by years of past interventions, the global energy system is left with zero structural buffer to absorb the deficit.

The extreme backwardation across the derivatives market proves that major industrial refiners are already panic-buying physical barrels here and now, rendering Wall Street’s paper speculation mere white noise. As supply chains constrict, financial markets are forced to confront an undeniable truth: fiat currency cannot be poured into a fuel tank, and virtual asset valuations will always yield to the laws of physical logistics.

The Death of Correlations: Why the Traditional 60/40 Portfolio Fails to Protect

For the global investment community, the current spike in energy prices signifies much more than expensive raw materials; it represents a systemic failure of foundational risk management models. For the past forty years, the bedrock of conservative investing has been the classic 60/40 asset allocation strategy (60% equities, 40% long-duration government bonds). This model relied on a reliable negative covariance: when the economy slowed and equities tumbled, capital fled into fixed income, driving bond yields down and prices up, thereby offsetting the portfolio’s drawdown.

Today, this mathematical relationship is officially broken. The destruction stems from the very nature of the underlying inflationary pressure. When inflation is driven by physical commodity supply constraints—energy, fuel, and logistics—rather than excess consumer cash, stagflationary pressure mounts. In this configuration, the correlation between stocks and bonds turns fiercely positive. They bleed together.

Supply-Side Shock (Energy Crisis)

│

├──► Rising Corporate Costs ───► Collapsing Net Income ───────► EQUITIES Fall

│

└──► Rising Inflationary Pressures ──► Surging Market Yields ──► BONDS Fall

The mechanics of this process are clear:

On the Equity Side: A rising barrel of crude automatically spikes operating expenses for every business across the board—from airlines and logistics operators to food manufacturers and tech giants maintaining power-hungry data centers. Logistical and raw material inputs climb faster than companies can pass them onto the end consumer. The result is an inevitable compression of net margins and a downward revision of corporate earnings guidance. Equities drop.

On the Bond Side: Oil at $95+ acts as a massive pro-inflationary catalyst. Fixed-income investors realize that sticky inflation will force central banks to keep benchmark interest rates elevated. In response, yields on long-duration government bonds (such as US 10-year and 30-year Treasuries) surge to price in the erosion of purchasing power. By the basic laws of debt markets, soaring yields mathematically mean the face value of the bond collapses.

Consequently, the passive investor holding a balanced index portfolio finds themselves pinned. The safety nets promised by academic economic textbooks are gone. Duration risk—the sensitivity of bonds to shifting interest rates—has evolved from an abstract academic metric into an immediate threat to capital preservation.

The Macroeconomic Trap: The Fed, a Resilient Labor Market, and Sticky Inflation

This unfolding commodity crisis is colliding with a highly complex domestic macro landscape in the United States. Friday’s official employment data (Non-Farm Payrolls) demonstrated unexpected resilience across the US economy. Job creation substantially outpaced consensus estimates, while the unemployment rate hovered near historical lows alongside accelerating hourly wage growth.

Under normal conditions, a robust labor market is interpreted by Wall Street as a green light—proof of a healthy consumer base. In the current context, however, these metrics have constructed a classic macroeconomic trap for the Federal Reserve. Tight employment means domestic consumer demand remains hot, inherently fueling sticky inflation within the services sector. When this domestic demand pressure is compounded by an external supply shock like $94+ oil, the regulator faces the immediate threat of an unanchored wage-price spiral.

The Monetary Regulator’s Macro Choke Point:

To cool inflation driven by surging oil and a hot labor market, the Fed is practically forced to maintain interest rates at a restrictive level (above 5.25%) or even consider further tightening. However, keeping rates higher for longer dramatically amplifies refinancing costs for the ballooning US national debt and places immense structural stress on the banking sector.

Central banks possess zero tools to physically widen shipping lanes or broker geopolitical truces. Monetary policy adjusts demand; it cannot manufacture supply. By raising interest rates, the Fed can force American consumers to purchase fewer vehicles or dine out less frequently, but it cannot force tankers to navigate faster or refineries to yield more diesel from scarce crude.

This structural friction thoroughly dismantles market expectations of a “soft landing.” Investors who built financial models on the assumption of rapid credit easing are now forced into emergency re-evaluations. Expensive capital has transitioned from a temporary hurdle into a long-term economic constant, automatically punishing valuations of high-multiple companies whose market caps were entirely predicated on future cheap money.

Logistical Choke Points and the Butterfly Effect in Global Supply Chains

Oil is not merely fuel for transport; it is the core infrastructure layer of global civilization. An energy shock of this magnitude never remains confined to local gas stations; it triggers a brutal butterfly effect across the entire value chain.

The first to absorb the impact is the global logistics sector. Ocean freight, which was only beginning to stabilize after years of disruptions, is facing a severe spike in bunker fuel costs. Major container carriers are already implementing emergency fuel surcharges, immediately inflating the landing cost of any physical good crossing the ocean. Furthermore, the necessity of rerouting shipping fleets away from hostile zones around the Middle East extends transit times between Asia, Europe, and the US by several weeks. This structural delay forces more vessels onto the water just to maintain previous cargo volumes, creating an artificial capacity deficit.

[ $94+ Crude Oil ]

│

├──► Surging Bunker Fuel Costs ───► Escalating Ocean Freight Tariffs

│

├──► Rerouting Around Choke Points ──► Extended Transit Timelines for Goods

│

└──► Expensive Naphtha/Petrochemicals ──► Higher Production Costs for Plastics

The second layer of impact hits heavy industry and petrochemical manufacturing. Crude oil is the direct feedstock for naphtha, the building block of polymers, plastics, synthetic fibers, and pharmaceutical inputs. A 15–20% surge in raw inputs over a compressed timeframe completely breaks the unit economics for chemical conglomerates. They are left with two options: pass these expenses down to customers (which dampens demand) or directly sacrifice their own operating margins.

Agriculture demands specific scrutiny. Modern high-yield farming is entirely tethered to energy prices. Diesel fuel accounts for a massive portion of harvesting and internal transit costs to grain elevators and ports. Moreover, natural gas and petroleum derivatives are critical inputs for nitrogen fertilizers. The June commodity shock sets up direct preconditions for a renewed wave of food-sector inflation by autumn, introducing structural margin risks for retailers.

Global supply chains, already complicated by deglobalization and market fragmentation, are proving highly fragile. In a world where primary manufacturing hubs are separated by thousands of miles, the escalating cost of moving physical mass through space becomes the ultimate brake on global economic output.

The New Capital Allocation Architecture: Where to Find Organic Yield

In an environment defined by macro reversals and broken correlations, holding onto legacy asset structures is equivalent to the slow burning of capital. Investors must pivot from strategies built around nominal growth under cheap credit toward preserving absolute purchasing power in a world of resource scarcity.

The primary beneficiary of this new capital allocation framework is the ultra-short duration debt segment. While long-duration bonds collapse under inflationary weight, short-term US Treasury bills (yielding above 5% with maturities under 6 months) offer a unique structural hedge. Because these instruments mature rapidly, they carry near-zero duration risk (interest rate sensitivity). In a highly volatile macro environment, parking capital in ultra-short T-bills provides maximum liquidity and guaranteed, risk-free cash flow, allowing investors to wait out the acute phase of the storm without risking capital erosion.

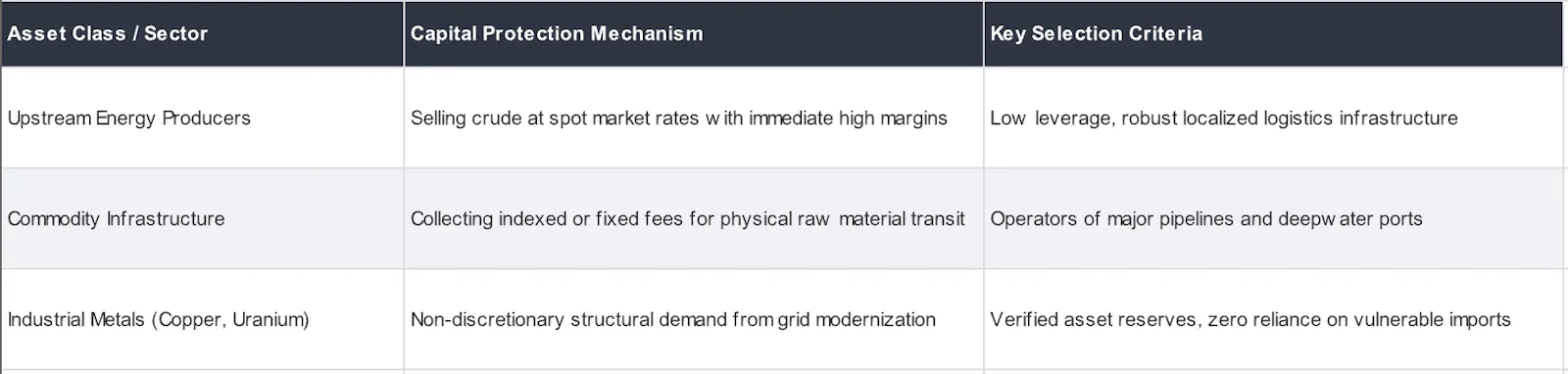

The second critical pillar is allocation to tangible assets with absolute pricing power. During structural inflation cycles, the supply of paper money is infinite, whereas the supply of physical resources is rigidly capped by nature and infrastructure capacity. Capital allocation must shift toward:

The definitive metric for equity selection in this climate is Free Cash Flow Yield and an enterprise’s capacity to self-fund operations and capex without relying on volatile debt capital markets. Companies weighed down by heavy debt loads taken out at floating rates will watch rising servicing costs completely erase top-line revenue growth.

Holding passive, broad-market indices (like the S&P 500) in June 2026 exposes capital to highly concentrated, unhedged operational risks. These indices remain heavily weighted toward sectors that historically underperform in a high-rate, expensive-energy environment. This structural regime shift demands an active, selective framework where physical reality, capital independence, and real margins dictate allocation. The era of financial engineering is yielding to the era of physical resource constraints, and capital will belong to those who calculate the true cost of tangible assets.

Date

09/06/2026