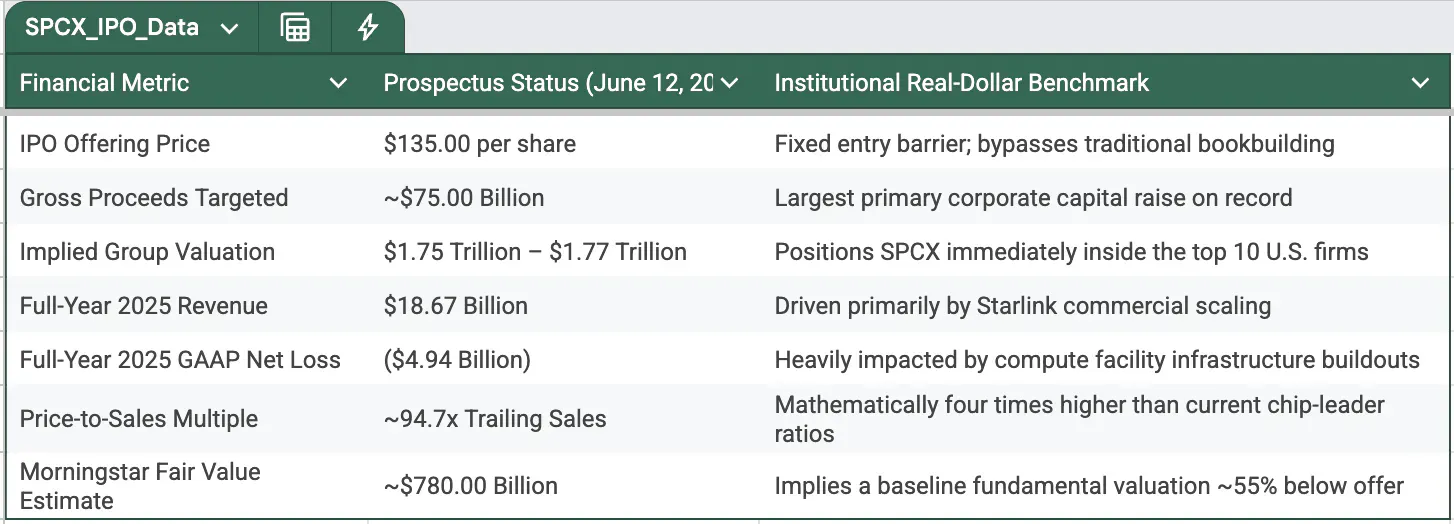

Today, June 12, 2026, SpaceX begins public trading on the Nasdaq under the ticker SPCX. The transaction structure is locked at a fixed price of $135 per share, targeting a historic gross primary raise of $75 billion across 555.6 million Class A shares. This establishes an implied market capitalization between $1.75 trillion and $1.77 trillion at the opening bell.

Elon Musk arrives at the 10th Annual Breakthrough Prize Ceremony held at the Academy Museum of Motion Pictures on April 13, 2024 in Los Angeles, California. Photo by Xavier Collin/Image Press Agency/Sipa USA)

The establishment media is already running the baseline narrative: a celebratory moment for retail investors to capture a generational slice of aerospace and artificial intelligence infrastructure. That framing is designed exclusively for retail clicks, not capital preservation.

When you strip away the corporate mythology, the registration filings reveal an unprecedented capital architecture. This listing is not designed for organic price discovery; it is a highly controlled liquidity event. Wall Street has engineered multiple operational backstops to suppress downside price action over the first 30 to 90 trading days.

1. The Capital Dislocation: IPO Metrics vs. Independent Valuation

The raw financial parameters of the amended S-1 prospectus present a stark structural contradiction. SpaceX is coming to market at an equity value that eclipses almost every mega-cap corporate listing in history, yet its internal balance sheet carries an accumulated deficit driven by heavy capital expenditure.

The core valuation metrics show exactly what public investors are being asked to underwrite:

These metrics confirm that at $135 per share, the public market is not pricing current operations. A trailing revenue multiple of 94.7x alongside a multi-billion dollar GAAP net loss means that capital is buying an options structure on long-duration future infrastructure capacity.

2. The Three Structural Mechanisms Suppressing Downside Discovery

The primary risk for any retail participant today is confusing an engineered price floor with organic market demand. The underwriting syndicate has locked down the public float through three specific operational mechanisms designed to prevent the stock from breaking below its issue price in the near term.

Mechanism 1: The Compressed Public Float

SpaceX is releasing a mere 4% to 4.2% of its total share base into the public float. The remaining 95.8% remains tightly restricted within insider tranches, with Elon Musk retaining over 82% of total voting control through a dual-class equity structure. By severely restricting tradeable supply, the underwriters can easily neutralize immediate sell-side pressure.

Mechanism 2: The 15-Day Index Fast-Track Loop

In May 2026, Nasdaq adjusted its index methodology to allow top-40 market-cap companies to qualify for the Nasdaq-100 after just 15 trading days, bypassing the traditional multi-month seasoning rules.

As a result, massive passive index vehicles like the Invesco QQQ Trust will become forced institutional buyers of SPCX before the end of June. Quantitative tracking data from Intropic indicates that index funds will mechanically absorb roughly 30% of the public float within the first three weeks of trading, creating an insulated demand loop completely detached from corporate fundamentals.

Mechanism 3: Tiered Lockups and Bank Greenshoes

The traditional 180-day lockup cliff has been replaced with a tiered structure where insiders can unlock an extra 10% allocation only if the stock trades above the $135 IPO price. Concurrently, the banking syndicate retains a 15% greenshoe option (representing an additional 83.3 million shares). If SPCX drops below $135, the syndicate will automatically buy shares on the open market to cover their short positions, effectively constructing an artificial buying floor.

3. The Segment Breakdown: Starlink Cash vs. Compute CapEx

To understand the internal cash burn, an Individual Sovereign must look past the consolidated revenue numbers and isolate SpaceX’s three primary reporting segments. The capital expenditures are highly uneven across the group:

Connectivity (Starlink): This is the fundamental anchor of current operations, generating 61% of total 2025 revenue ($11.4 billion) and tracking a highly profitable $4.4 billion in operating profit. The subscriber base has successfully scaled past 12 million across 160 countries.

Space (Commercial Launch/Starship): Bounding over 80% of domestic rocket launches, this segment retains a dominant 90% commercial market share but operates as a capital-intensive utility with negative net earnings due to ongoing Starship deep-space research and development.

Artificial Intelligence (Compute Infrastructure): This segment represents the true source of balance sheet friction. The subsidiary structure absorbed 61% of total group capital expenditure in 2025, expanding to 76% of all CapEx in Q1 2026. This aggressive burn is driven by the rapid construction of massive supercomputer facilities like the 1-million-GPU Colossus 1 facility.

While massive cloud agreements with Anthropic ($1.25 billion monthly) and Alphabet ($920 million monthly) guarantee long-term recurring revenue layers, the near-term costs of acquiring and powering over 110,000 Nvidia GPUs have pushed group free cash flow deeply into negative territory. Operating losses in Q1 2026 alone accelerated to 75% of full-year 2025 deficits, confirming that the business is expanding its infrastructure spend far faster than its current cash collections can offset.

4. The Sovereign Directive

For Individual Sovereigns managing capital for long-term financial autonomy, the largest IPO in history requires absolute execution discipline over emotional momentum.

First, I am not deploying capital into SPCX at the $135 listing price. The engineered mechanisms detailed above are highly likely to stabilize the stock during its initial trading window. However, an artificial floor is not a margin of safety. Paying a 94x trailing revenue multiple for an enterprise carrying a negative free cash flow profile fails to clear our strict risk-reward thresholds.

Second, recognize the passive capture rule. If you hold a standard Nasdaq-100 index fund or retirement vehicle, your capital is already buying SpaceX today. Your passive allocations will automatically absorb shares at whatever price the syndicate maintains during the 15-day fast-track window. There is no operational need to duplicate that exposure in your active ledger.

Third, wait for genuine price discovery to mature. The true valuation test begins later this summer when the underwriting greenshoe protections expire, the initial forced index buying concludes, and the first tiered insider lockup tranches become eligible for liquidation.

Independent institutional modeling from Morningstar places the core fundamental fair value of the satellite and launch assets closer to $780 billion, or roughly $60 per share. We will let the institutional funds battle over the speculative story premium at $135. Our tactical window opens only when the artificial floor drops, the corporate mythology clears, and the raw mathematical data supports an entry on our own terms.

Disclaimer: This analysis is for educational purposes only and should not be considered investment advice. Always do your own research before making investment decisions.

Items marked with an asterisk (*) are promotional and help support this newsletter at no cost to readers.

Datum

12.06.2026