True market navigation requires ignoring sentiment shifts and focusing entirely on structural liquidity flows. When the financial press screams about a Friday sell-off, institutional desks don’t look for emotional triggers — they map the sudden repricing of risk across the yield curve. The unyielding upward momentum that defined the start of 2026 hit a definitive macroeconomic wall over the weekend, proving once again that capital allocation is dictated by monetary parameters, not retail enthusiasm.

We are entering an operational window governed by severe cross-asset rebalancing, geopolitical friction, and accelerating bond market volatility. Below is your objective, data-backed intelligence brief to protect your principal and position your portfolio ahead of the opening bell.

1. What Happened This Weekend: The Anatomy of a Market Dislocation

The public markets just closed out their most brutal operational window of the year, breaking key technical support lines across the board.

US Markets: The End of the Winning Streak

On Friday, the unyielding upward momentum of the broader indices was violently halted. The S&P 500 snapped its historic 9-week winning streak, dumping 2.6% in a single session. The technology sector bore the brunt of the liquidation cascade: the tech-heavy Nasdaq Composite plunged 4.2% (a historic single-day point drop of over 1,121 points).

The primary catalyst was the May non-farm payrolls report. The data revealed the addition of 172,000 new jobs—exactly double the consensus expectations of mainstream economists. In a standard economic environment, robust labor metrics indicate strength; in a highly leveraged macro environment, it confirms structural heat. Fixed-income desks immediately adjusted their models, pricing in a hawkish Federal Reserve that will keep interest rates higher for longer, with money markets now pricing in a distinct probability of an additional rate hike before the end of 2026.

Tech Sector & Crypto: AI Guarantees Under Scrutiny

The semiconductor space led the downward spiral. Broadcom issued forward sales guidance for its AI chip division that failed to satisfy the market’s hyper-inflated expectations, triggering an immediate industry-wide selloff. However, behind the public market volatility, the private venture capital space demonstrated massive scale: Anthropic finalized a staggering $65 billion funding round (boosting its valuation to a massive $900 billion) while concurrently filing confidentially for a Q4 IPO.

Simultaneously, Microsoft expanded its enterprise moat by debuting its native “OpenClaw” AI business agents alongside an Nvidia-powered “Dev Box” architecture. In the digital asset space, Bitcoin moved in near-perfect lockstep with legacy tech, dropping 2.5% over the weekend to settle near $62,160, proving once again that crypto remains a high-beta liquidity proxy rather than an isolated hedge.

Geopolitics & Domestic Friction: The Ceasefire Collapses

The fragile geopolitical balance in the Middle East shattered over the weekend. Iran launched a direct missile strike targeting southern Beirut, Lebanon. Late Sunday evening, President Trump attempted an intervention, publicly stating he was urging Israeli PM Benjamin Netanyahu to halt further military escalation, noting that “both sides have done their part.”

The diplomatic backchannel failed. Within hours, the Israeli military executed retaliatory strikes against core military installations deep within western and central Iran, elevating regional conflict risks to critical levels. Domestically, political friction worsened as President Trump abruptly walked out of a pre-recorded NBC Meet the Press interview following a sharp debate with Kristen Welker regarding election transparency and the potential deployment of an “anti-weaponization fund” to compensate January 6th defendants.

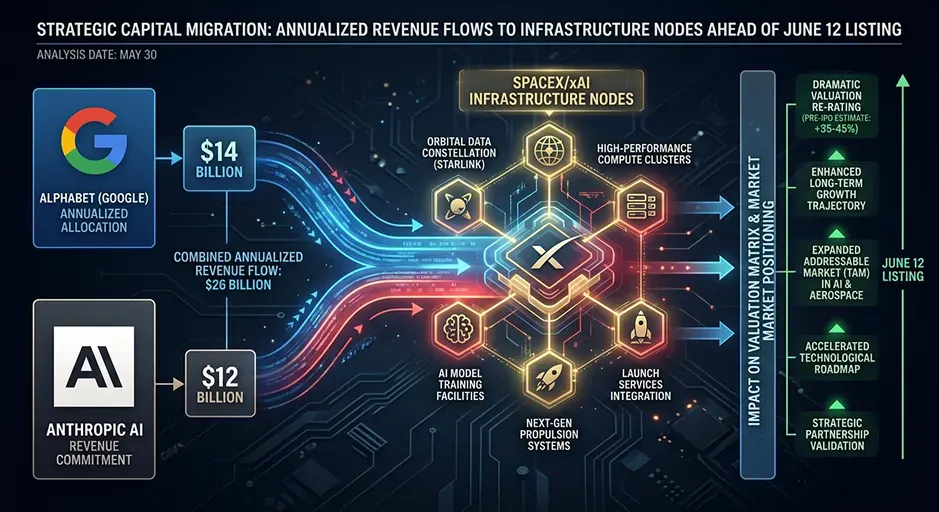

2. The SpaceX IPO Prospectus: Tracking the $30 Billion Google Compute Catalyst

While public tech equities bled on Friday, the private corporate infrastructure landscape underwent a structural transformation that completely alters the calculus for the upcoming June 12 SpaceX IPO.

On June 5, SpaceX amended its S-1 IPO filing to disclose a massive, multi-year Cloud Service Agreement with Alphabet's Google. The hard math of the contract changes everything:

The $920 Million Monthly Premium: Google has legally contracted to pay SpaceX $920 million per month from October 2026 through June 2029. If carried to full term, this single cloud architecture deal transfers $29.4 billion directly onto SpaceX’s balance sheet.

The Infrastructure Footprint: Under the terms of the agreement, SpaceX is leasing access to a massive cluster of roughly 110,000 Nvidia GPUs, alongside custom CPUs and enterprise memory banks. This represents over 100 megawatts of brute-force AI infrastructure—enough to power 75,000 homes simultaneously — deployed as bridge capacity to scale Google’s Gemini Enterprise platform.

The Combined Institutional Floor: This transaction drops immediately after Anthropic locked up SpaceX’s Memphis “Colossus 1” facility for $1.25 billion per month. On an annualized baseline, just these two enterprise compute deals yield over $26 billion in recurring revenue. To contextualize this: this infrastructure leasing layer alone brings in more annual revenue than SpaceX’s entire 2025 business footprint from Starlink and launch services combined.

The Fine Print and Gating Risks

Sovereign investors must look past the $30 billion headline and dissect the operational clauses inside Amendment No. 2. First, the contract features strict delivery performance metrics: if SpaceX fails to deliver the full 110,000 GPU cluster by September 30, 2026, Google has the immediate right to terminate the contract or force a severe pro-rata reduction in fees. Second, after December 31, 2026, either party can exit the arrangement entirely via a simple 90-day mutual notice clause.

Furthermore, Google is not just a client; it is an insider, holding roughly a 5% equity stake in SpaceX post-xAI merger. Simultaneously, the two tech giants are actively negotiating “Project Suncatcher”—a collaborative blueprint to launch Google’s experimental test databases directly into orbit as decentralized, satellite-based data centers.

The strategic implications for the IPO are clear: Musk is actively pivoting SpaceX from a capital-intensive aerospace manufacturer into a high-margin, recurring-revenue AI infrastructure powerhouse targeting a $1.77 trillion market valuation ($135/share across 555.6 million Class A shares). However, the filing also revealed that a select 5% “friends and family” share allocation worth $3.75 billion will have zero lockup restrictions and can liquidate immediately on day one, reinforcing our strategy of tactical patience during listing week.

3. What to Expect This Week: Volatility Testing the Floor

The upcoming macro calendar contains high-impact catalysts that will dictate whether this correction deepens or stabilizes.

The US Inflation Print (Wednesday, June 10)

The Bureau of Labor Statistics will drop the May Consumer Price Index (CPI) report on Wednesday. This is indisputably the most critical data deployment of the month. Following Friday’s unexpectedly hot employment metrics, an inflation print that lands above consensus will fundamentally lock in the Fed’s hawkish stance ahead of the critical June 17 policy meeting, potentially forcing a prolonged capital retreat out of growth equities.

The European Central Bank Mandate (Thursday, June 11)

The ECB is widely anticipated to execute a hawkish 25-basis-point interest rate hike, lifting its benchmark deposit rate to 2.25%. Frankfurt’s hand is being forced by rising imported inflation risks, driven directly by surging crude oil prices resulting from the direct Israel-Iran military exchanges.

Futures and Sector Rebalancing

Early Monday futures show equity indices attempting to establish a temporary technical floor, but energy and defense complexes are seeing heavy institutional buy-side volume as crude spikes. Expect technology equities to remain highly defensive and acutely sensitive to any upward movement in the US 10-Year Treasury yield.

4. The Sovereign Directive: Tactical Navigation Rules

When index volatility spikes, the baseline mandate for an independent portfolio remains unyielding: maintain absolute capital preservation and avoid chasing emotional swings.

Insulate Growth Exposure: With the Nasdaq showing historical point volatility, do not add capital to extended growth names until the post-CPI bond yields stabilize. Let the passive index-selling run its course.

Harvest Volatility Premiums: High market anxiety means options implied volatility is expanding rapidly. This environment is highly lucrative for selling premium—look to establish cash-secured puts on premier semiconductor and defense leaders at strikes 10–14% below current spot prices.

Hedge with Commodities and Energy: As long as the Middle East missile corridor remains active, energy assets act as a structural hedge for your equity risk. Ensure your capital structure includes direct exposure to hard assets that absorb geopolitical shockwaves.

The systems governing public markets are designed to transfer capital from undisciplined hands to patient, institutional operators. When macro data and geopolitical events collide, your only true shield is a cold, calculated strategy. Read the data, respect the technical lines, and execute your plan with absolute precision. Let’s get to work.

Data

09/06/2026