Apple Intelligence reboots with "Project Campo." The premium harvesting opportunity is live.

“Efforts and courage are not enough without purpose and direction.”

– John F. Kennedy

Real market navigation requires ignoring sentiment shifts and focusing entirely on structural liquidity flows. When the financial press screams about a “thoughtful and long-term” succession plan inside the world’s largest corporate balance sheet, professional options desks don’t read the press releases—they map the sudden repricing of risk across the implied volatility smile.

Today at Apple’s annual WWDC event, Tim Cook delivers his final keynote as chief executive. On September 1, 2026, he officially hands the corner office to John Ternus, Senior VP of Hardware Engineering, and transitions to Executive Chairman. Behind the polished media statements, Apple is undergoing its most profound leadership shakeup since 2011, with four senior executives across AI, software design, and legal frameworks leaving the bench.

For Individual Sovereigns holding AAPL or looking to deploy capital, this leadership transition—combined with an emergency AI reset—creates an exceptional window to extract consistent monthly income. Let’s strip away the corporate marketing and audit the raw balance sheet data and options parameters for the week ahead.

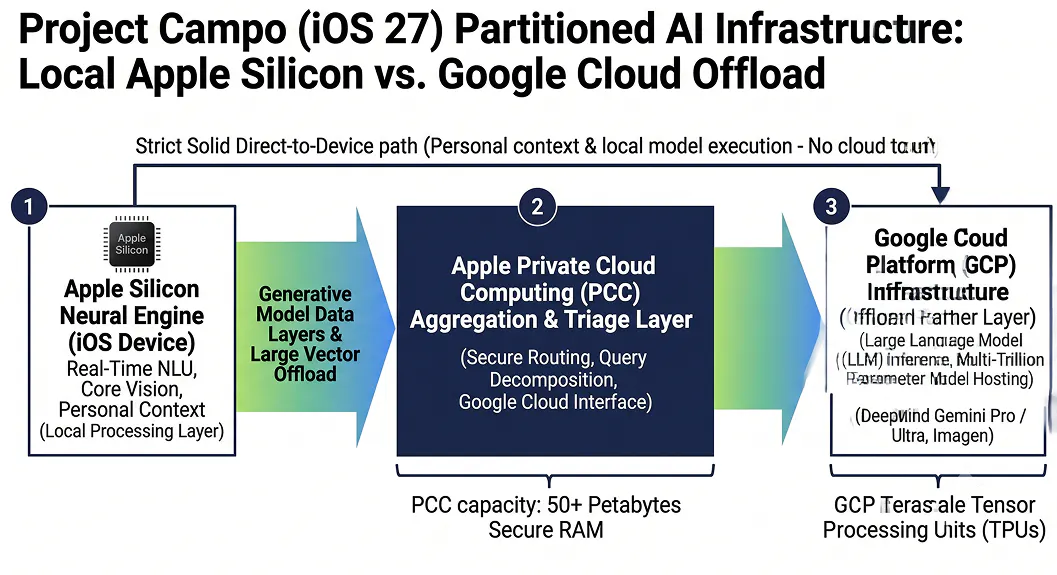

1. The AI Credibility Deficit: Project “Campo” vs. Competitor Cloud Fees

The original Apple Intelligence architecture, unveiled in 2024, has spent two years facing heavy institutional criticism over recurring delays and compromised software execution. While Google’s Gemini and OpenAI’s multi-modal agents rapidly captured enterprise market share, Apple remained trapped in a reactive development cycle.

Tonight’s keynote targets an aggressive overhaul of Siri under the internal code-name “Project Campo” (slated for iOS 27). The mandate for the incoming CEO is clear: transition Siri from a basic voice utility into an autonomous, cross-application intelligent agent that holds multi-modal context. However, the operational fine print reveals an expensive infrastructure reality: to compute heavy generative prompts, Apple must integrate external Gemini models and route core processing to Google’s data centers.

While sell-side desks like Morgan Stanley maintain a 65% base-case probability of stock upside into the $365–$385 range (and $440 in a bull case) upon a flawless demo, smart money is focused on margin preservation. AAPL closed at $307.34 on June 5. While that gap looks attractive on a chart, renting competitor infrastructure introduces massive, recurring cloud operational costs that did not exist two years ago. Institutional capital flows reflect this underlying friction: large funds poured $287 billion into the stock over the last cycle, but simultaneously pulled out $131 billion. The elite desks are actively hedging.

2. Institutional Friction: Dissecting the Options Chain

Apple operates in an ecosystem where mega-cap asset managers control the primary float, with institutional ownership sitting at a massive 67,73%. Vanguard controls a 1.43 billion share block, State Street holds 601 million shares, and Berkshire Hathaway retains an exposure worth over $61 billion. When you trade AAPL, you are navigating an order book written by these heavyweights.

Recent quarterly SEC 13F filings reveal a distinct lack of institutional consensus heading into Cook’s exit:

The Liquidators: Prominent asset managers including Chelsea Counsel Co. (down 10.3%) and Town Capital LLC (down 8.1%) systematically trimmed their exposure on concerns over executive turnover.

The Accumulators: Conversely, Northern Trust Corp expanded its position by 13.3%, and Connors Investor Services aggressively accumulated shares, elevating AAPL to its second-largest holding.

This divergence represents a textbook institutional conflict priced directly into the options chain. The convergence of a major binary AI event, a CEO transition, and large-scale fund rebalancing has pushed short-duration Implied Volatility (IV) to premium levels. While market makers price in structural doubt, sovereign investors harvest it.

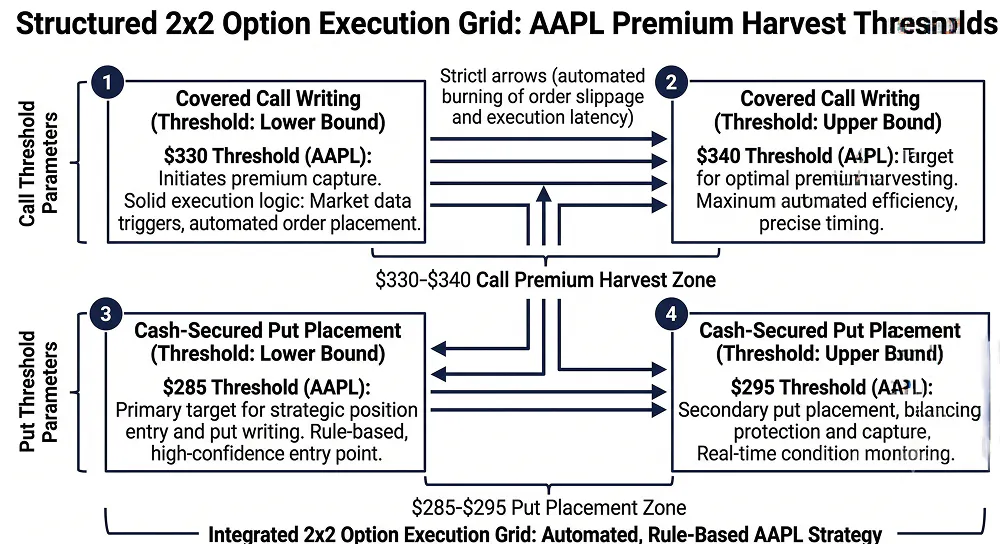

3. The Tactical Strike Plan: Capitalizing on the AAPL Transition

With AAPL trading near the $307.34 baseline, we deploy a conservative, yield-enhancing options framework designed to convert this macro volatility into direct liquidity.

Strategy 1 — The Covered Call Harvest: If you currently hold a foundational block of AAPL shares, write monthly covered calls in the $330–$340 strike range (roughly 7–10% out-of-the-money). This allows you to capture the inflated pre-WWDC volatility premiums. If a stellar Siri demo drives a rally to $330, you capture the equity upside and keep the cash premium. If the software execution underdelivers and the stock trades sideways, the premium behaves as an immediate cushion, lowering your net cost basis. This is how you systematically engineer a Sovereign Paycheck.

Strategy 2 — The Cash-Secured Put Entry: To accumulate Apple shares with an institutional margin of safety, sell cash-secured puts down at the $285–$295 strike parameters (4–7% below current spot price). You collect immediate cash income for your willingness to acquire the asset on a localized pullback. If assigned, you secure equity at a cost basis that accounts for the leadership transition. If the stock stays elevated, you retain the premium as pure profit.

Operational Risk Guardrails: Never over-allocate more than 5–7% of total investment capital to a single equity setup. Enforce strict exit rules before the opening bell. Post-WWDC, closely monitor the next 10-Q filing for any accelerating cloud infrastructure expenditure tied to external AI server routing—that specific line item will tell you the absolute truth about Apple’s margins long before management discusses it on an earnings call.

4. The Sovereign Directive

As Tim Cook takes the stage for his final WWDC keynote as CEO, he will project absolute confidence. He will present features engineered to convince the market that Apple’s hardware-software ecosystem is insulated from structural disruption. I respect his historical corporate execution. However, professional capital does not run on respect. It runs on verified filings, probability-weighted setups, and raw arithmetic.

The incoming executive suite inherits an ecosystem at a massive crossroad: an artificial intelligence strategy dependent on competitor infrastructure, a thinning executive bench, and structural disagreement among tier-one institutional holders. This boardroom friction is not our concern—it is the raw material we use to construct our financial independence. Treat the volatility with mathematical discipline, capture the options premium, and pay yourself first on your own terms. Position your capital accordingly.

Data

09/06/2026